Global markets rally on US and China sentiment.

The combined economic output of the United States and China accounts for approximately 40% of the global economy. Key stimulus in the world’s two largest economies has been a major catalyst for financial market movements in the third quarter.

The US Fed cut its main interest rate by 50 basis points for the first time in more than four years – with more cuts likely to come – ending a long run of interest rates at a two-decade high, with the aim of slowing the US economy enough to stamp out high inflation. As US inflation subsided from its peak, Jerome Powell said the Fed can now focus more on keeping the labour market solid and the economy out of a recession.

In China, the People’s Bank of China (PBOC) unleashed one of the country’s most daring policy campaigns in decades to pull the Chinese economy out of deflation, bolster the property market and achieve the government’s 5% GDP growth target. The stimulus included interest rate cuts, freeing-up cash for banks, as well as liquidity support for stocks and the promise of something “fiscal” in yet-to-be-defined size.

China’s $17 trillion economy has struggled through a painfully slow recovery following the coronavirus pandemic. The country was very aggressive in its Covid-era restrictions and has been very cautious in easing those restrictions as infections declined. The result has been complicated. Domestic demand declined sharply, while the country’s factories and mines generated huge surpluses. Attempts to export those surpluses at reduced prices have many economies – such as the US – raising tariffs and other barriers, to prevent China from “exporting its deflation,” which has become a common term in political parlance.

The greater stimulus measures from China together with the market pricing an aggressive US Fed easing cycle, bode well for risk assets. The global interest rate cutting cycle also continued to broaden as many central banks – including the South African Reserve Bank (SARB) – cut and/or commenced cutting rates. Hence, we saw the US equity market steamrolling ahead, with new record highs, and a big quarter-end rally in Chinese and other emerging market exchanges. The MSCI World Index was up another 6.5% in Q3 and the MSCI Emerging Market Index, of which China represents almost 30%, surged 8.8%.

US…kicks off easing cycle

Over the six easing cycles since 1989, there were only two periods where the Fed managed to avoid an immediate economic downturn – the first in 1995 and the other in 1998. This time, US equity and bond markets are anticipating that the Fed will get a 1995-style soft landing, where it successfully controls inflation without sacrificing employment, and where growth remains positive. Back then, Alan Greenspan cut rates to 5.25% from 6% in just six months, cooling the economy without it ‘slipping’ into a recession.

At this stage it would be reasonable to assume a cut of at least 25bps at each of the two remaining Fed meetings in 2024 and that the Fed will be aiming to cut rates at a steady pace over the next two years to get the target interest rate down to around 3% by the end of 2026. During this phase, the Fed will also be hoping that the economy can keep growing at around 2% and that the unemployment rate remains steady in a range of 4% to 4.5%.

Historically, US equity markets have shown strong performance during Fed rate-cutting cycles, particularly in the absence of a recession. This suggests that rate cuts by the Fed, when not accompanied by an economic downturn, generally create a ‘risk-on’ environment, driving equity gains. However, it is important to recognise that no two cycles are identical.

AI fever has loosened its grip

The ‘Magnificent Seven’ has grown to represent more than 30% of the total S&P 500 market capitalisation. New York Magazine called this ‘the greatest concentration of capital in the smallest number of companies in the history of the US stock market.’ However, in the past quarter it brought a new order to markets. Investors began to look sceptically at heavy spending on AI by big tech companies and the narrative switched to, ‘are they going to make money with all this spending?’ It was a recipe for the broadening of a rally that many investors worried had grown precariously reliant on a few big tech shares.

The S&P 500 Index gained 5.9% in Q3 and is up 22% YTD. Sectors ranging from industrials to financials gained 10%, while utilities gained 17% – all outperforming technology which was flat for the quarter. Value shares beat growth shares and small-capitalisation stocks emerged to leave their large-cap peers in the dust.

Bonds also rallied

Bond investors also enjoyed a rally, as the Fed’s rate cuts finally began. The yield on the benchmark 10-year US Treasury Note – which falls when prices rise – dropped to 3.7% from 4.3% at the end of June, to snap a two-quarter streak of rising yields. Overall, the Bloomberg Barclays Global Aggregate Index gained 7% in Q3.

The quarter held an interesting development in government bonds. Two-year US Treasuries had been trading at a higher yield than 10-year notes, a phenomenon known as an inverted yield curve that has been a classic recession signal, since July 2022. Then in early September, the inversion disappeared, as the longer-term Treasury’s yield finally climbed back above that of the shorter-term note. An inverted yield curve sometimes returns to normal just ahead of a recession, as traders bet on aggressive rate cuts from the Fed. But many investors are optimistic – more than 50% of respondents to Bank of America’s September global fund manager survey said they did not expect a US recession in the next 18 months.

China…growth remains under pressure

Economic growth in China came in lower than expected in Q2, indicating that the economy was struggling to maintain momentum. GDP growth increased by 4.7%y/y, the slowest growth in five quarters as efforts to boost consumption activity have been disappointing. This despite numerous measures to boost growth as a protracted property sector slump and weak domestic demand have restrained economic activity and consumer prices. The annual CPI rate was up only 0.6% in August 2024, falling short of market forecasts of 0.7%.

The automobile industry in China is a good example of the challenges the economy is facing. Motor dealerships across China are facing massive losses – about 138 billion yuan ($19.6 billion) for the first eight months of 2024 alone, according to the China Automobile Dealers Association, as consumers hold off on making major purchases. This is a classic example of deflation when the consumer waits for prices to fall further before making a purchase. The country’s best-selling automobile brand, BYD Co., embarked on a series of price cuts at the start of the year, the latest in a brutal round of cost cutting that has been going on since the beginning of 2023 in an effort to get consumers to buy more vehicles.

Biggest equity market rally in a decade

Equity markets rallied after authorities unveiled measures (see below) to bolster the economy. The MSCI China soared 23.6% for the quarter and is up 29.6% YTD. The index lost more than 50% of its value from 2021 to 2023, highlighting how China’s slowing economy has thumped investor confidence.

No bazooka …but a step in the right direction

The stimulus includes more than $300 billion in measures, mostly via monetary – as opposed to fiscal – channels. A short summary of the latest stimulus package follows.

The market welcomed the latest stimulus but cautioned that it does not represent the bazooka that many see as needed to get consumers in China to increase spending. Doubts remain whether it was enough to break China’s longer-term deflationary pressure and entrenched real estate crisis.

Policymakers are pulling out the stops

Then the BIG surprise. Two days after the central bank’s surprise stimulus, pledges from the Politburo to boost growth show an unusually high degree of urgency and determination to support the economy. While the Politburo offered no specifics on FISCAL SPENDING, Reuters reported that the Ministry of Finance is planning to issue 2 trillion yuan ($284 billion) of special sovereign bonds this year. That funding will be evenly split between stimulating consumption and helping local governments tackle debt problems.

Japan…rates on hold

The Bank of Japan (BoJ) kept interest rates steady at its last meeting, signalling it was in no rush to raise borrowing costs further. This after the central bank raised the cost of borrowing for only the second time in 17 years in July, as it tries to normalise monetary policy in the world’s fourth largest economy. The BoJ increased its key interest rate to ‘around 0.25%’ from the previous range of 0% to 0.1%.

The Nikkei 225 Index was down 4% in Q3 after the market dropped 4.8% on the last day of September. The new prime minister Shigeru Ishiba, who has been critical of the Bank of Japan’s easy policies in the past, favoured normalising interest rates. Higher interest rate typically strengthens the yen and puts pressure on Japanese stock markets, which are heavily weighted by exporters. A strong yen would make their exports less competitive.

UK/Europe…inflation slows

The Bank of England kept its main interest rate on hold at 5%, after cutting the interest rate by 25bps to 5.0% in August – the first time in more than four years. On the other hand, the European Central Bank has cut interest rates once again, lowering its deposit rate by 25 basis points. While inflation is cooling, growth indicators have remained concerning.

Local Market

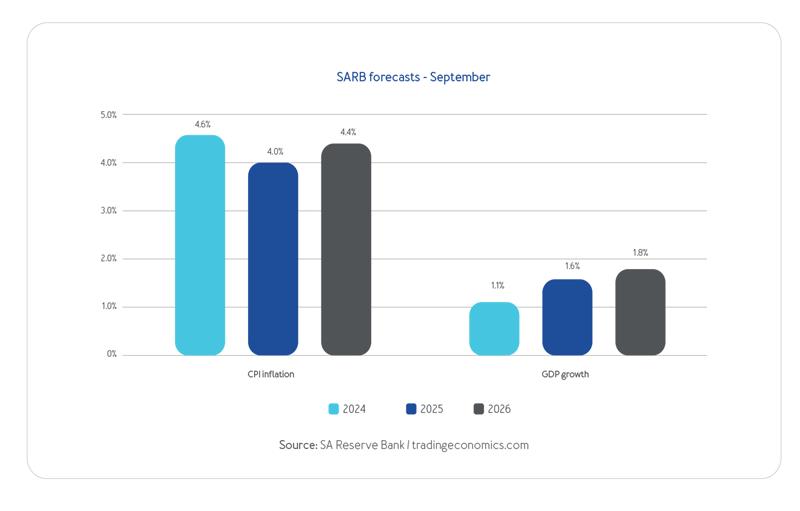

The SARB decided to cut the Repo rate by 25bps to 8% at its last meeting. Prior to the decision the Repo rate had been unchanged at 8.25% since May 2023. The market expects a further 25bps cut in November 2024 and more rate cuts are certainly on the way. The inflation outlook has improved, and the SARB’s official forecast suggests inflation will be somewhat below the 4.5% target over the next two years, together with a moderate improvement in growth.

The rand improved further against other major currencies and ended the quarter at R17.26 to the dollar, as investors continued to lean towards riskier assets – the recent interest rate cut from the US was among the biggest drivers for the firmer rand. The rand has appreciated almost 10% against the dollar over the past 12 months.

Equity market rallied

The local market benefitted from increasing positivity following the start of the interest rate cutting cycle and optimism around SA’s Government of National Unity (GNU). The JSE All Share Index surged by almost 10% in Q3, led by financials (+14%) and industrials (+11%), where China-exposed tech investors Naspers and Prosus have led the advance. Resources were marginally negative, losing 1%, despite a late surge at quarter end as authorities in Beijing took steps to stimulate the economy. A strong Chinese economy will boost demand for commodities, which will help South Africa’s mining exports.

The listed property sector also rallied and is up 30% from a total return perspective for the year to date to 30 September 2024. It is the top-performing asset class on the JSE, having been boosted by the latest interest rate cut and no load shedding by Eskom for six straight months. The two largest listed property companies, Growthpoint and Redefine, are up 15% and 24% respectively for Q3 2024. The sector saw a decline with equity raised dropping to R7.4 billion in 2023 from R69.4 billion in 2014. This year there has been decent activity with Vukile Property Fund raising R1 billion and Sirius Real Estate £150 million (approximately R3.4 billion) from SA and offshore investors. Members of the SA REIT Association are reporting improved fundamentals, declining vacancy rates, rental increases – albeit off a low base – and demand for space in key locations.

Strong performance from the bond market

SA bonds continued to perform well in Q3 driven by the GNU frenzy that started in June, a lower inflation print in August and most recently, interest rate cuts. Bond yields across the curve fell 130bps in Q3 as investors remained optimistic about the fiscal outlook post the formation of the new coalition government. The All Bond Index returned 10.5% for the quarter, fuelled by the rally in the 12-plus area of the curve, which gained 14.2%. Over the past year, the ALBI is up an impressive 26.1%.

In conclusion – growing optimism

The GNU recently passed its first 100 days, and the report card is broadly positive. The new government has notched up several successes and helped embed a sense of optimism that we may be able to achieve meaningful economic reform. We know the challenges are massive but if the positive sentiment is to last, this should not stop us from working together and translating all the ideas and plans into actions.

Albert Louw

INN8 Invest