Global stock markets are scaling record heights. From Wall Street to Hong Kong investors are cheering — the mood is euphoric, and the bulls are in control.

With indices at record highs, a pervasive sense of complacency is sparking caution among some investors who suggest that global equity markets appear disconnected from underlying economic challenges and have raced ahead of fundamentals. US markets continue to rise, although stagflation is considered a significant risk. Europe’s major indices are riding the wave, yet growth indicators remain tepid. China’s manufacturing rebound is uneven and fresh US tariffs introduced in August, are just beginning to filter through to Asian exporters.

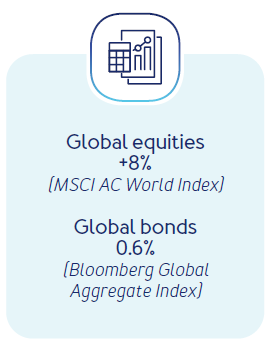

| Global stock markets are scaling record heights. From Wall Street to Hong Kong investors are cheering — the mood is euphoric, and the bulls are in control. With indices at record highs, a pervasive sense of complacency is sparking caution among some investors who suggest that global equity markets appear disconnected from underlying economic challenges and have raced ahead of fundamentals. US markets continue to rise, although stagflation is considered a significant risk. Europe’s major indices are riding the wave, yet growth indicators remain tepid. China’s manufacturing rebound is uneven and fresh US tariffs introduced in August, are just beginning to filter through to Asian exporters. These cross-currents are also evident in currency markets. The US dollar’s path is pivotal to global markets. The US dollar has been the world’s principal reserve currency and is the most widely used for international trade. A sudden strengthening would tighten financial conditions worldwide and squeeze merging markets that have benefitted from easier funding this year. The DXY Dollar Index, which tracks the strength of the dollar against a basket of major currencies, extended declines, losing 10% year-to-date. The US dollar has softened on rate-cut bets, but any hawkish shift from the US Fed — or another round of tariff escalations — could send it higher and unsettle risk assets across global markets.The MSCI AC World Index gained a solid 8% in Q3 in dollar terms, up 17% YTD. The MSCI Emerging Market Index was up 11% in dollar terms and 28% YTD, led by Chinese tech shares.Bond markets were volatile throughout the quarter as global political uncertainty and concerns around fiscal sustainability came into focus. Nonetheless, the Bloomberg Global Aggregate Bond Index ended the quarter up 0.6%, as US Treasuries rallied and credit spreads tightened. |  |

The US economy proved resilient. The final estimate of second-quarter GDP growth came in stronger than expected, at 3.8%, versus a prior estimate of 3.3%. A record downward revision to annual US employment growth, paired with no surprises in the latest inflation data, sealed the deal for the Federal Reserve to cut interest rates by another 25bps for the first time this year. Tariffs have yet to push up inflation as much as many had feared but there is a real risk that markets are underestimating the potential inflationary impact of tariffs that could still come down the tracks.

Government shutdown

Funding for federal agencies lapsed on 1 October, after Congress was unable to pass a stopgap bill to prevent a government shutdown. In a shutdown, government offices continue essential work, but tasks deemed non-essential come to a halt. Salaries are not paid, and many workers are laid off until congress passes new funding.

The most recent government shutdown during Trump’s first administration, began in December 2018 and lasted more than a month. It was the longest in US history and reduced annualised GDP growth by 0.4% in the first quarter of 2019. A full shutdown could more closely mirror the effects of the 16-day 2013 funding lapse, which lowered annualised growth by as much as 0.6%, the Office of Management and Budget reported.

Bull market continued its risk-on run

The S&P 500 Index has pushed to fresh highs fuelled by investor optimism for rate cuts, solid corporate earnings and ongoing AI euphoria, up another 8% in Q3. The Nasdaq Composite gained 11% and the rally has broadened to beaten-down shares poised to benefit from lower borrowing costs. The Russell 2000 Index, which tracks smaller US companies, recently closed at its first all-time high since 2021, up 12% in Q3.

Growth shares continued to outperform value by a slim margin, even as value shares rebounded from the second quarter. Communication services stocks climbed 12%, while technology was up 13%. Consumer defensives were the only sector in the red, with losses of 2.7%. For Q3 2025, the estimated earnings growth rate for the S&P 500 is 7.9% y/y, according to FactSet.

The market is instantly rewarding AI spending

| The euphoria towards artificial intelligence is creating a strange kind of new math in the share market. Investing heavily in AI infrastructure, even before concrete returns are realised, creates a speculative environment where an increase in market capitalisation is directly tied to AI-related investments and pronouncements. By way of an example, Nvidia Corp. announced it will buy a $5 billion stake in rival Intel Corp. and plans to invest up to $100 billion in ChatGPT creator OpenAI. The chipmaker added more than $320 billion in market value in the three trading days when the plans were announced, triple the amount the company is expected to spend under both agreements. Alibaba’s share price jumped 10% after the company said it would spend more on AI than the $50 billion target set earlier in the year. The news resulted in their market capitalization increasing by more than $35 billion. Other stocks that have seen a lift this year after pledging to spend more than $317 billion combined on AI include Meta Platforms Inc., Microsoft Corp., Alphabet, and Amazon.com, whose gains account for a major part of the rally in the S&P 500 Index in 2025. Together, the four have seen their market capitalisation boosted by about $1.8 trillion. Alphabet Inc. subsequently joined an elite group of companies valued at more than $3 trillion, the latest sign of improving investor sentiment toward the Google parent. |  |

Oracle Corp. is another beneficiary of plans to boost spending on AI, alongside high-profile partnerships with the likes of OpenAI, SoftBank Group Corp. and Meta Platforms. The company is expected to spend $35 billion on capital expenditure in fiscal year 2026. The share price has risen by more than 80% this year, adding nearly $390 billion to its market value.

These massive increases in market value come even as only a few companies have been able to show a material return on the investment in their financials. While massive corporate spending plans typically have not tended to be instantly rewarded in the share market, these moves highlight that investors are still happy to keep piling into shares of those companies spending big on data centers to position themselves as leaders in this space. While technological infrastructure investment has drawn scepticism in the past due to unfavourable outcomes such as the bursting of the dot-com bubble, there is more support today for innovations that have already proven to be transformational.

The European Union and the US finalised a trade framework in July, establishing a 15% tariff ceiling on most EU goods — a rate less severe than initially feared but still higher than hoped. The US and EU economies account for almost a third of global trade.

The ECB kept interest rates unchanged in August at 2.15%, following seven consecutive cuts. ECB President, Christine Lagarde, said the Central Bank was in “wait-and-see” mode, awaiting more clarity on future US/EU trade relations. German inflation figures came in higher than expected for July, potentially signalling renewed inflationary pressures that could influence ECB policy.

France, the new ‘bad boy’ of Europe

France, the second largest economy in the EU after Germany, is the new poster child for fiscal distress, taking over a role long played by Italy. In Q3 France suffered two sovereign downgrades, just as Italy won its first upgrade from Fitch Ratings since 2021, underscoring doubts the country can deliver on promises to tame its debt during a period of political instability. Short-term causes for concern about Paris are clear — prevailing instability since the elections last year, missed deficit targets and no clear path to fiscal consolidation. In addition, parliament is divided into irreconcilable factions and France is now on its fifth prime minister in less than two years.

France posted the largest fiscal deficit of the Eurozone in 2024 and is likely to do so again in 2025, according to Morningstar, even if it meets its own target of 5.4% of GDP — far above the EU’s 3% limit.

Inflation surprised on the upside in July, and although the Bank of England cut its policy rate by 25bps, the accompanying hawkish tone reduced market expectations for further easing. A weakening labour market and fragile consumer confidence weighed on sentiment.

China’s economy grew 5.2% in Q2 despite US tariffs. Q2 was boosted by government stimulus and a temporary pause in the US-China trade war, which allowed exporters to rush out shipments ahead of new tariffs. The US and China extended their trade truce until November, reducing near-term trade risks.

China’s industrial production lost momentum in July with growth momentum projected to continue weakening for the remainder of this year amid mounting headwinds including trade tensions, deflationary pressures (CPI dipped 0.4% in August y/y), and persistence in the prolonged property downturn.

The latest deceleration in industrial production was impacted by a moderation in vehicle production, which grew at its slowest pace since October 2024. Chinese authorities signalled that they would continue to take a measured approach to stimulus with a focus on managing over-capacity and addressing the ‘disorderly competition’ among businesses that is adding to the deflationary trend in the economy. China is sending its world-beating auto industry into a tailspin. Government policies that prioritise production targets over market demand have led to over-investment by motor manufacturers. Excess vehicles have created ‘lose-lose’ transactions throughout the sales chain and many Chinese dealers are not able to make money because of excess inventory. Subsequently, dealers have responded by slashing prices, fuelling the deflationary dilemma.

Strong equity market led by tech shares

China continued to drive emerging market sentiment. Beijing announced ambitious plans to triple chip supply by 2026, boosting local technology shares. The Hang Seng Tech Index climbed 22% in Q3 and 46% YTD. The index has been on a strong upward trajectory, driven by grassroots AI advancements that gained global attention following surprising breakthroughs by startup DeepSeek.

The elevated momentum in tech shares marks a sharp reversal from just a year ago, when the sector was weighed down by regulatory crackdowns and a slowing economy. New impetus came from the government’s announcement of increased support for the sector, alongside Alibaba Group Holding Ltd.’s plans to ramp up AI spending and its new partnership with Nvidia Corp. to use its training tools for robotics and self-driving vehicles.

A weaker yen supported export-oriented shares in the market, and the Nikkei 225 Index jumped 12% in Q3. A US/Japan trade deal, which lowered US tariffs on almost all Japanese exports from 25.0% to 15.0%, combined with resilient domestic macro data and ongoing corporate governance reforms, contributed to the outperformance of Japanese equities.

Tariffs — received our ‘letter’

The US government notified Pretoria that Washington had introduced a hefty 30% tariff on South African imports. However, minerals considered critical to the US — notably platinum group metals (PGMs), gold, chrome and coal — will attract 0% tariffs. That accounts for about half of what SA exports to the US, so excluding these commodities is a major relief. Where SA will really feel the pain is on the export of cars, already 25% (previously 0%), steel and aluminium, now 50% (previously 25% and 10%) and agricultural products at 30% (most products previously entered the US duty-free), which means that SA wines in the US will be considerably more expensive.

SARB holds rates as the bar for easing has been raised

The South African Reserve Bank (SARB) kept borrowing costs unchanged at its last meeting in September after a 25bp cut in July, maintaining the benchmark interest rate at 7%. This after data showed inflation unexpectedly slowed to 3.3% in August from 3.5% the prior month.

The SARB appeared concerned that the recent improvement in inflation dynamics has not yet translated into better anchored expectations. SA inflation is expected to move back to around 4.5% over the next 12 months with several factors becoming less supportive such as a decline in the fuel price, a strong rand and China exporting deflation. Understandably, the credibility of SA monetary policy will be tested if a sustained 3% inflation rate, which they are now aiming for, cannot be achieved on a persistent basis. In the short term, the SARB has acknowledged the importance of clear and credible communication in anchoring inflation expectations and thus getting inflation lower, highlighting the need to finalise the target reform with the National Treasury as soon as possible.

Growth outlook remains fragile

South Africa’s economic growth outlook for 2025 is projected to be fragile, with GDP expanding only slightly — insufficient enough to significantly reduce the already high unemployment rate. This low growth is attributed to our ongoing inability to address structural challenges. Fixed investment is essential for economic growth but achieving this requires investor confidence, which is fostered by business-friendly policies, stable regulatory environments, and the consistent addressing of key challenges like energy and corruption.

Gold and platinum shares have stolen the show on the JSE

| The market hit a new record in Q3. The JSE All Share Index gained 12.8%, led by the resources sector, which was up a staggering 47%, with the big investment story this year being the surge in precious metals. AngloGold Ashanti and Gold Fields were up 47% and 72% respectively in Q3 together with platinum shares, Valterra Platinum (up 59%) and Implats (up 38%). Domestically focused companies — the socalled SA Inc stocks i.e. banks and retailers —remain under pressure. Retailers had a very good 2024 and benefitted from lower interest rates, lower inflation and the two-pot money. Year to date, the JSE All Share Index gained 28.9%. It is, however, important to mention that similar to the S&P 500 Index, the local rally is fuelled by a narrow group of shares. |  |

Gold has soared 47% this year. The story for gold remains — central bankers are buying and there is geopolitical uncertainty. For centuries, gold has been the go-to haven asset in times of political and economic uncertainty. Its status as a reliably high-value commodity that can be transported easily and sold anywhere, offers a sense of safety when everything else is in turmoil. Investors have sought refuge in gold amid President Trump’s expanding trade war, record US debt levels, and growing infringement on the independence of the Federal Reserve. Investors have also piled into gold-backed exchange traded funds, with total holdings in mid-September reaching their highest point since 2022, according to data collected by Bloomberg. Also, historically gold has been negatively correlated with the US dollar. Because gold is priced in dollars, when the greenback weakens, gold becomes cheaper for holders of other currencies. The dollar reached a three-year low against other major currencies in July and remained subdued until quarter end.

Prosus acquisitions

Tech share Prosus, the largest by market capitalisation on the local bourse, gained 22% in Q3 and 61% YTD. The group recently posted a profit outside of its Tencent stake and aggressively looks for acquisitions to put its cash at work. The strategy is to deploy AI and large e-commerce models to accelerate growth across its business units that include online food delivery, classifieds, payments and fintech.

In Q3 Prosus, which is owned by OLX Group BV, agreed to acquire La Centrale, a leading motors classifieds platform in France for €1.1 billion. The deal will strengthen OLX’s European motors portfolio given that La Centrale boasts strong brand recognition and scale. The market opportunity is also compelling as the French car market is healthy and resilient with solid growth potential in the dealer segment. The deal will accelerate the growth of Prosus in Europe, where it is set to close a €4.1 billion transaction for JustEat Takeaway.com.

Corporate activity

• Anglo American Plc agreed to acquire Canada’s Teck Resources, creating a company worth more than $50 billion, in one of the biggest mining deals in more than a decade.

• Billionaire Jannie Mouton’s foundation in a R7.2 billion Curro buyout.

• The Competition Tribunal gives the nod to the Barloworld takeover.

• Canal+ received SA competition approval for the R52.7 billion MultiChoice deal, which cleared the way for the largest pay-tv and streaming business on the continent.

Investors snapping up bonds

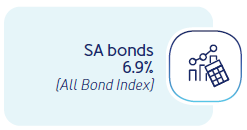

| The All Bond Index gained 6.9% in Q3 and 14% YTD. The bond rally has been supported by inflation that eased to a five-year low and geopolitical noise seems to have quietened down for now. Yields on SA benchmark bonds extended declines in Q3 with the 10-year yield on the Government bond ending the quarter 80 bps lower at 9.1%. Foreign investors are snapping up South African bonds as they seek out higher real yields. The local bond rally received a boost with the decision by JPMorgan Chase & Co. to diversify its flagship emerging market index, and divert investor flows away from heavyweight debt issuers like China and India. They are expected to gradually lower the issuer cap on its GBI-EM Global Diversified Index in the first half of 2026. Money market assets gained 1.8% in Q3 and 5.7% for the year-to-date. |  |

Client Service & Practice Management