In the world of investments, “diversify” is a drumbeat that echoes from trading floors to retirement seminars, championed as one of the most prudent ways to manage risk.

Introduction

In the world of investments, “diversify” is a drumbeat that echoes from trading floors to retirement seminars, championed as one of the most prudent ways to manage risk. You have likely read countless articles on why it is smart not to put all your eggs in one basket, across stocks, asset classes, industries, and geographies.

But there is a curious paradox. In investment circles, everybody lauds diversification. Yet so many portfolios remain dangerously narrow in one aspect – the people who manage the assets and their decisions. Diversification of asset managers is a strategy that is often overlooked but can be as important as diversifying into new markets or currencies. After all, each manager carries their own assumptions, motivations, and blind spots. These ‘idiosyncratic risks’ can compound in ways that traditional measures of diversification do not address. Idiosyncratic risk is tied less to the broader market and more to the specific mindset or methodology of the manager.

A multi-dimensional approach

When we say “diversify,” what usually comes to mind?

These elements form the cornerstone of traditional portfolio allocation. Yet true diversification is not just about these big buckets, it also lives in the more subtle, often less discussed layers namely the biases, risk tolerances, and decision-making processes of the people making the investment calls.

The ‘human factor’ in portfolio construction

Think of a portfolio manager as you would think of a chef. They each have their signature ingredients (preferred asset classes), cooking style (investment philosophy), and approach to seasoning (risk tolerance). Some might be minimalists, committed to a single elegant strategy, such as pure value or growth. Others might be experimental gastronomists, mixing in unorthodox instruments and derivatives to enhance returns. Each approach may be valid, but also brings very specific, and sometimes unrewarded, risks.

Examples may include:

Idiosyncratic risk often goes unrewarded

The premise of diversifying across asset classes is to capture different market risk premia. Over the long run you should produce returns from various ‘return streams’ i.e. shares, bonds, property and so forth. However, idiosyncratic risks from a particular manager’s style or biases often do not carry a systematic ‘premium’ that you can exploit. Instead, those risks can be more akin to quagmires of human error. If a manager, for instance, systematically overestimates earnings growth in cyclical industries, investors will not necessarily be compensated for that risk in the form of higher returns. That is an unrewarded risk you would be better off neutralising.

By diversifying across multiple managers, you effectively spread your exposure to a range of perspectives and methods. While you might end up forgoing the dramatic outperformance of a single star manager whose idiosyncrasies happen to work out brilliantly one year, you are also more insulated from underperformance if those biases backfire.

A choir of voices

Visualise your investment pool as a choir. Each singer (manager) brings a unique voice – soprano, alto, tenor, bass. In a multi-manager setup, it is not about one singer dominating with a show-stopping solo, it is about the harmony that arises from multiple, well-curated voices. When all members have distinct yet complementary vocal ranges and skills, the performance becomes richer, fuller, and less reliant on a single virtuoso.

Similarly, if every manager in your stable is a ‘growth at all costs’ devotee, that would be like having an entire choir of sopranos. It might be thrilling when hitting a high note in a market that rewards growth, but it can become unbearable when the market turns. Diversifying managers means adding baritones and mezzos, so your total ‘portfolio performance’ does not collapse when the market decides to favour slower tempos or deeper tonalities.

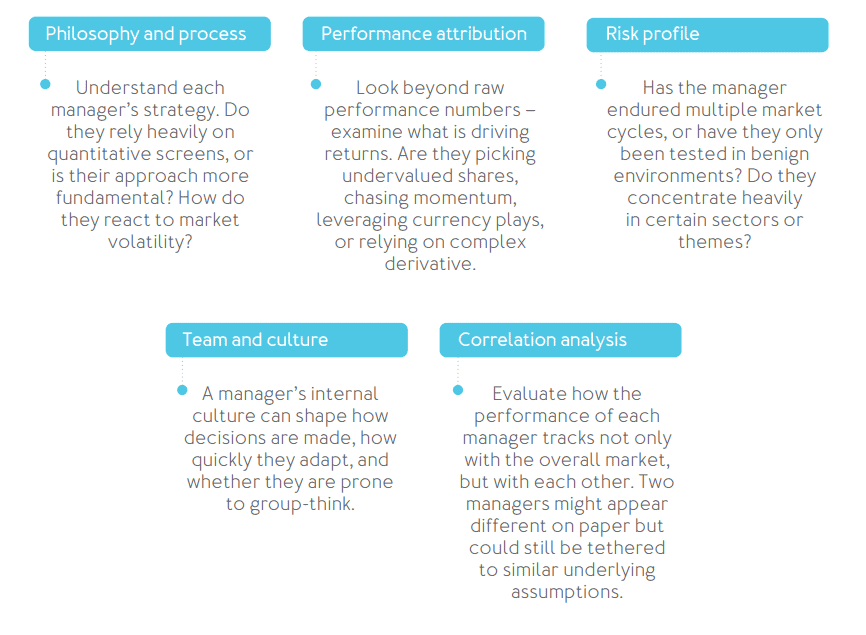

Investment due diligence

How do you ensure you are bringing genuinely different ‘voices’ into your investment choir? Start with the same rigour you would use for an asset class:

Operational due diligence

Operational due diligence (ODD) is as crucial as investment due diligence itself. It goes beyond assessing performance or investment philosophy, critically examining the structural integrity that underpins the ability of a manager to consistently deliver their intended strategy. To comprehensively mitigate hidden risks, operational due diligence must rigorously evaluate the quality, depth, and reliability of the manager’s operational environment.

While ODD may lack the glamour of investment performance analysis, rigorous ODD forms a critical defensive layer, enabling the multi-manager strategy to deliver its value effectively.

Why a multi-manager model works

Beyond blunting idiosyncratic risks, a multi-manager approach offers two additional benefits:

Dynamic flexibility. Having multiple managers means you can more fluidly rebalance capital based on changing markets. For instance, if one manager runs a high-yield bond strategy and another focuses on equities, you can shift allocations as opportunities ebb and flow.

Alignment with goals. Different managers can serve different roles in your overall plan. Some focus on generating stable income while others chase long-term capital growth or alternative strategies. In this sense, you can align managers with the varying objectives you might have for different pockets of capital.

A new way to think about diversification

Far from being an extra or nice-to-have, diversifying managers is central to robust portfolio construction. It acknowledges that no one has perfect foresight or an infallible method. By blending multiple perspectives, you guard against unforced errors tied to a single individual’s peculiar way of seeing the world.

Sure, you may get lucky. A lone wolf manager might deliver jaw-dropping returns for a few years. But star power can fade with market shifts, and the unwatched ‘idiosyncratic’ exposures could become traps. When you build your portfolio with a multi-manager mindset, you are effectively mitigating that single-point-of-failure risk, just like you would do by mixing large capitalisation with small capitalisation shares or domestic shares with international ones.

Conclusion

The bottom line is that diversification extends well beyond merely holding an array of asset classes, industries, or currencies. True diversification includes blending varied managerial approaches to avoid loading up on a single worldview. When building a portfolio, remember that managers, like markets, can harbour hidden risks and biases. By diversifying your managers just as rigorously as you diversify your assets, you create a more nuanced and resilient investment environment – one poised to weather the idiosyncrasies of human nature as effectively as it weathers the storms of market cycles. Each manager comes with their own set of assumptions, philosophies, and biases, and those are as fundamental to a portfolio’s risk profile as interest rates or market cycles.

Investing wisely often comes down to anticipating what might go wrong before it does. Apart from just spreading your ‘bets’ across different asset buckets, remember to also spread them across different minds and methods. In this way, you strengthen the foundation of your investment strategy – reducing your vulnerability to any one person’s quirks, no matter how brilliant or compelling they might seem in the moment